eviews interpretation results

Running a PP test using the TBILL series using the Andrews bandwidth. The serial correlation LM test results for this equation with 2 lags in the test equation strongly reject the null of no serial correlation.

Eviews Training Basic Estimation Basic Regression Analysis Eviews

EViews Gareth EViews Moderator.

. Determines whether or not an independent variable is irrelevant to the regression ie. Error of each independent variable. Not depicted here are the results for the joint tests and the test regression equation.

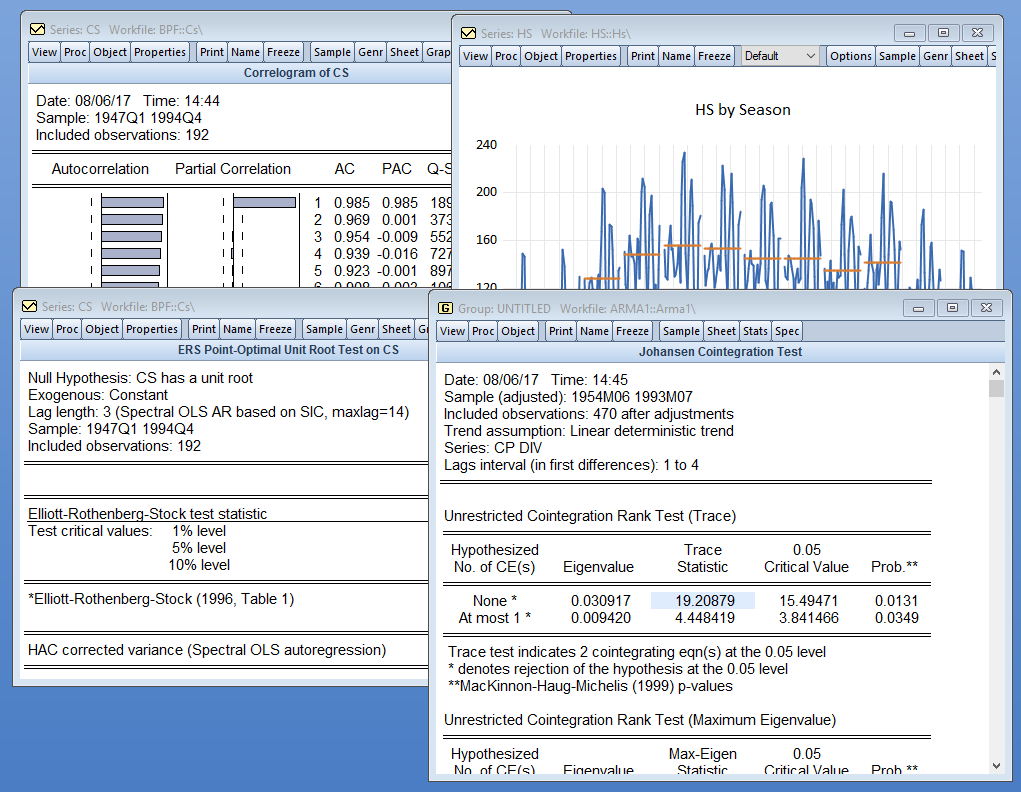

Your cointegration order is equal to one if each of the. 2863613 10. Since your test statistic is much lower than all of the critical values you can reject H 0 at a significance level 1.

3435299 5. An introduction to performing statistical analysis in EViews. Now you need to compare this with the critical values under H 0.

Multiple Series Statistical Analysis. I am trying to estimate unrestricted VAR but when to. EViews reports the test statistic along with output from the corresponding test regression.

EViews offers several seasonal unit root tests including the classical Hylleberg et al. Hello I am new in econometrics and so in Eviews. It also gives an understanding of the basic features of a regression out.

For these tests EViews reports the uncorrected estimate of the residual variance and the estimate of the frequency zero spectrum labeled as the HAC corrected variance in addition to the basic output. The test statistic is 3722113. For econometric discussions not necessarily related to EViews.

Two cointegrating vectors is not the same as cointegration order being equal to two. This is probably a really simple question for those of you who have used this test before but I am getting rather confused. EViews displays a variety of results in the output view following estimation.

The first probability is for the f statistic test for ommitted variables which comes out. This brief hands-on tutorial shows how to interpret a regression output in EViews10. C 3 and C 4 is for the ARCH term but the absolute value in C 3 is for the effect of the.

The top portion of the output displays information about the optimization technique ARMA estimation method the coefficient covariance calculation and if requested the starting values used to initialize the optimization procedure. As I read the results you have two cointegrating equations or two cointegrating vectors. Here we specify spectral intercepts and use defaults.

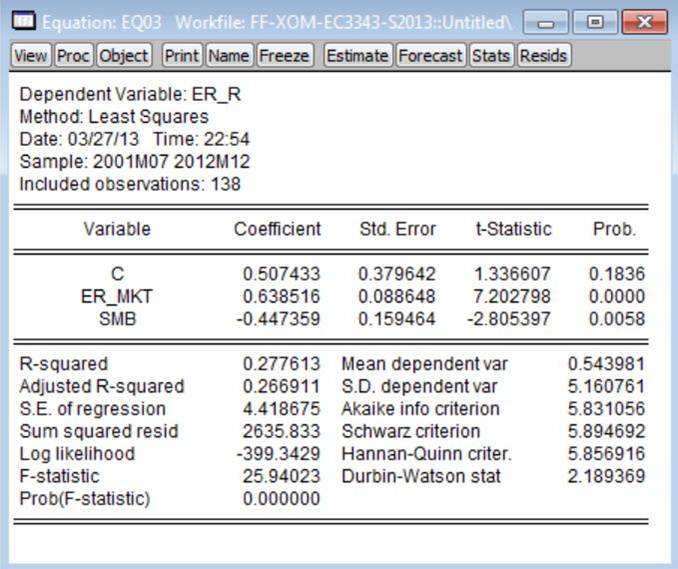

The results presented in Table4show a significant relationship between dxt and dyt with a good coefficient of determination5 Adjusted R2 around 063 and without autocorrelation of order one6 25 Validation Our OLS regression satisfies all. Estimated coefficients - 2 std error is the 95 confidence interval. Single Series Statistical Analysis.

EViews provides tests for serial correlation normality heteroskedasticity and autoregressive conditional heteroskedasticity in the residuals from your estimated equation. Indicates the likely sample variability and hence reliability. The coefficient is 0.

Although not every statistical procedure is discribed this tutorial should provide enough understanding to get you started. This tutorial shows to run a regression in Eviews and the interpretation of the regression outputThere are other videos on data analysis in SPSS as linked b. In this tutorial i will show you how to estimate apply ARDL and how to interpret it.

The critical values are given with. This translates into cointegration rank being equal to one number of variables in the system minus the number of cointegrating vectors. Next consider the Canova-Hansen test performed on the same data.

1990 test the Smith and Taylor 1999. ARCH term is the square of past residual factors e2 while GARCH is the past volatility variance H for general GARCH model and in the case of E-GARCH it is the past values of log variance H. Wed Feb 20 2013 1012 am.

Below are the some of the pre-requisite conditions which must satis. Absolute t-stat values of 2 or more mean the 95 confidence interval of the. This tutorial is divided into two sections.

You are right C 5 is for the GARCH term. This is using eviews 7 I have asked it to perform whites test and these are the results I recieved. This tutorial shows how to run a correlation in Eviews and how to interpret the correlation outcomeOther related data analysis videosRegression analysis in.

Powerful Analytics

The Simple Linear Regression Model By Using Eviews Hkt Consultant

Eviews10 Interpret Regression Output Stataoutput Eviewsoutput Interpret Regressionoutput Youtube

8 Eviews Result For Arch Lm Test Download Table

Statistics Of Garch 1 1 Model With Arma 1 1 In Eviews Download Scientific Diagram

Eviews 11 New Features Estimation

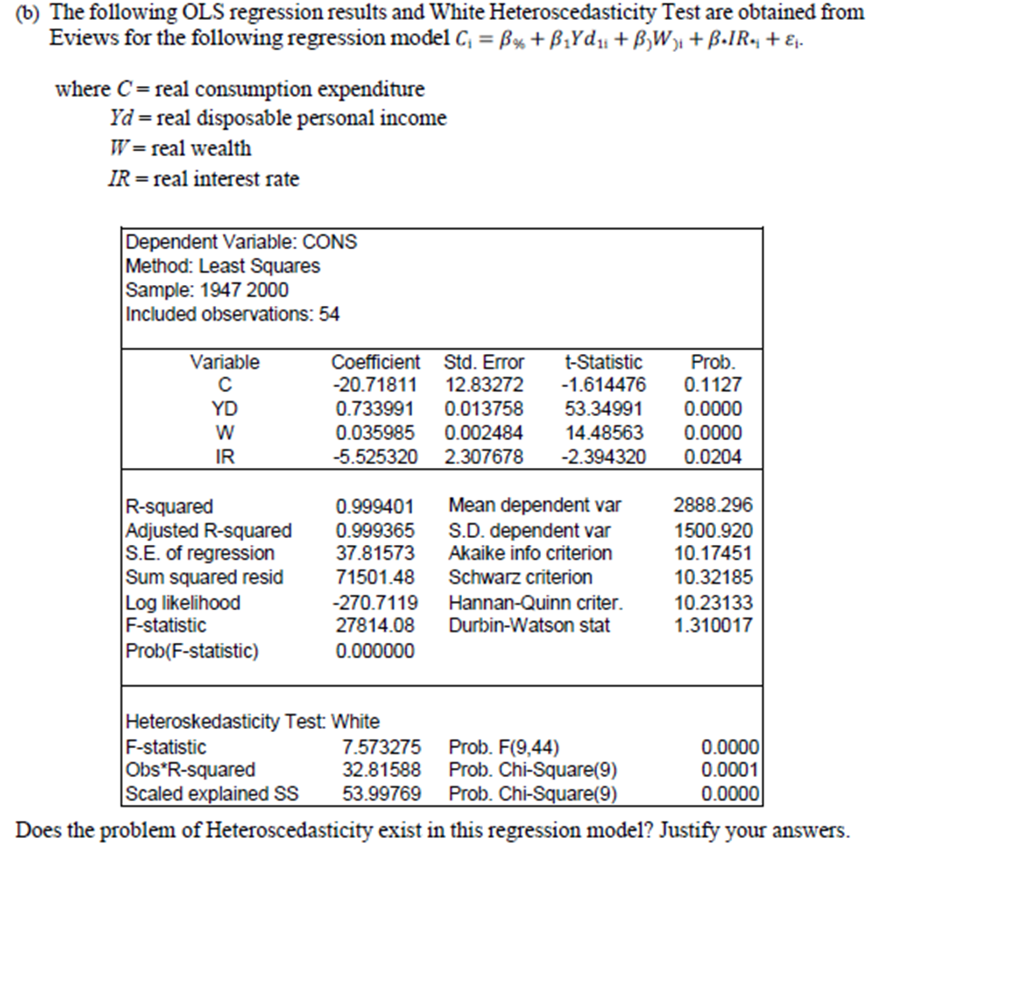

Solved 6 The Following Ols Regression Results And White Chegg Com

Eviews 7 Interpreting The Coefficients Parameters Of A Log Lin Model Youtube

Powerful Analytics

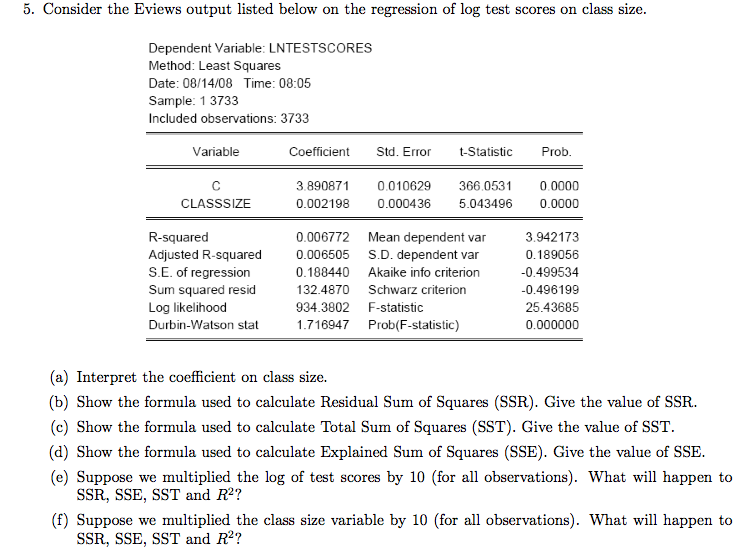

Solved Consider The Eviews Output Listed Below On The Chegg Com

Powerful Analytics

Time Series Linear Regression Analysis Output Interpretation In Eviews Youtube

Powerful Analytics

Econ 3343 Course Project

Eviews 11 New Features Estimation

Eviews Training Basic Estimation Basic Regression Analysis Eviews

3 Eviews Output For Multiple Regression Model Estimates Download Table

Eviews 12 New Features Estimation

Eviews 12 New Features Estimation

0 Response to "eviews interpretation results"

Post a Comment